1.Policy & Infrastructure Gaps

Despite strong service-sector growth, the Philippines continues to face structural bottlenecks in infrastructure and governance. Transport systems are congested, logistics costs are high, and energy supply remains unstable. These weaknesses raise the cost of doing business and limit competitiveness compared to regional peers. Policy execution also lags, with reforms often delayed or inconsistently applied.

2.Structural Weaknesses

Although the Philippines has achieved strong economic growth, productivity improvements remain weak. Over 90% of growth since 2010 has been driven by capital investment rather than productivity gains, with total factor productivity contributing less than 10%. Growth has largely occurred in non-tradable sectors with lower productivity potential, while declining export competitiveness, regulatory barriers, skills shortages, slow technology adoption, and climate-related disruptions continue to constrain productivity growth.

3.Weak Manufacturing Base

The Philippines has not developed a strong manufacturing sector compared to its ASEAN peers like Vietnam or Thailand. Much of its industrial activity is limited to low-value assembly, with heavy reliance on imported raw materials and components. This weak base prevents the country from fully integrating into global supply chains, reducing its ability to attract large-scale foreign investment in advanced industries.

4.High Import Dependence

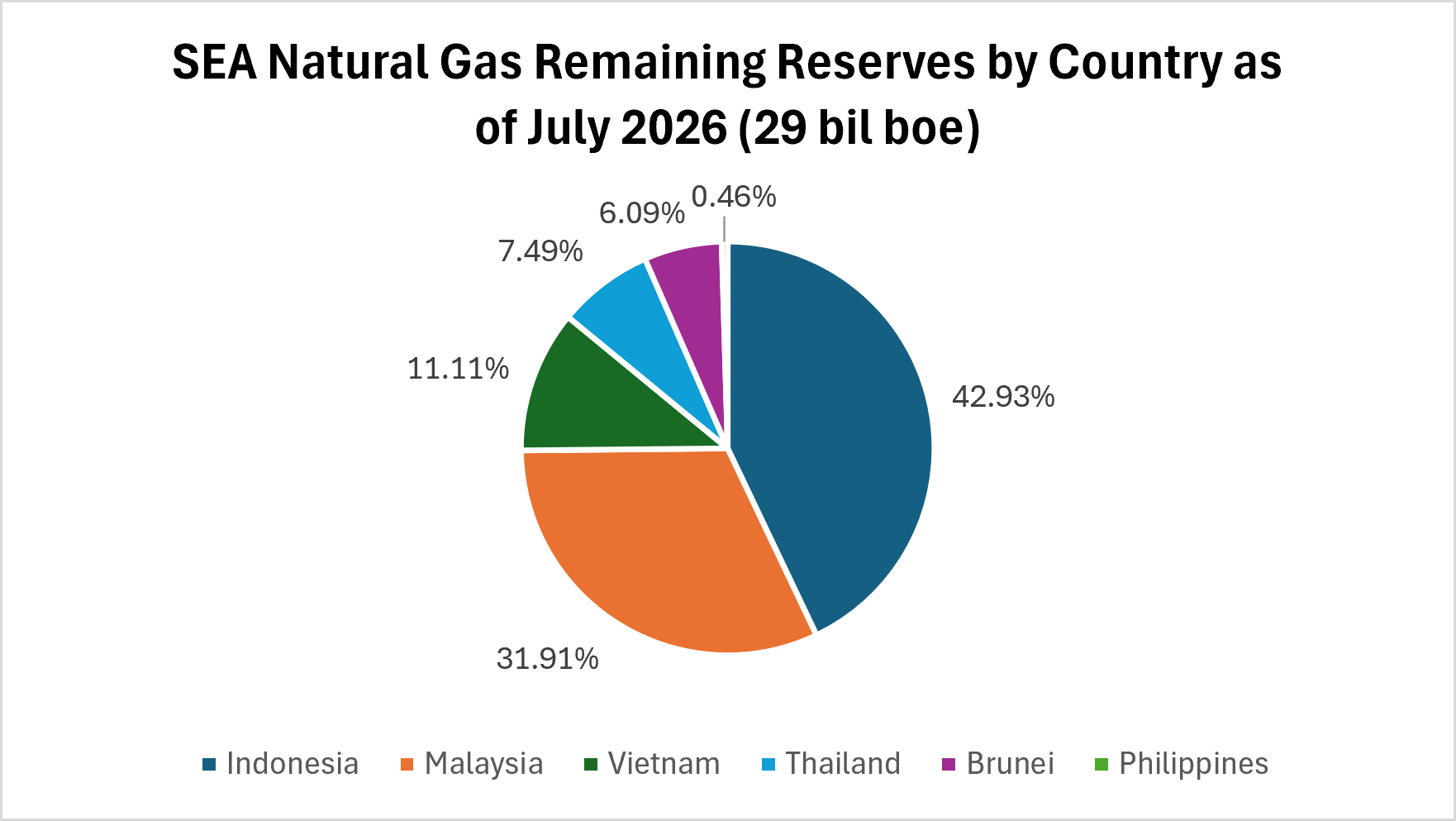

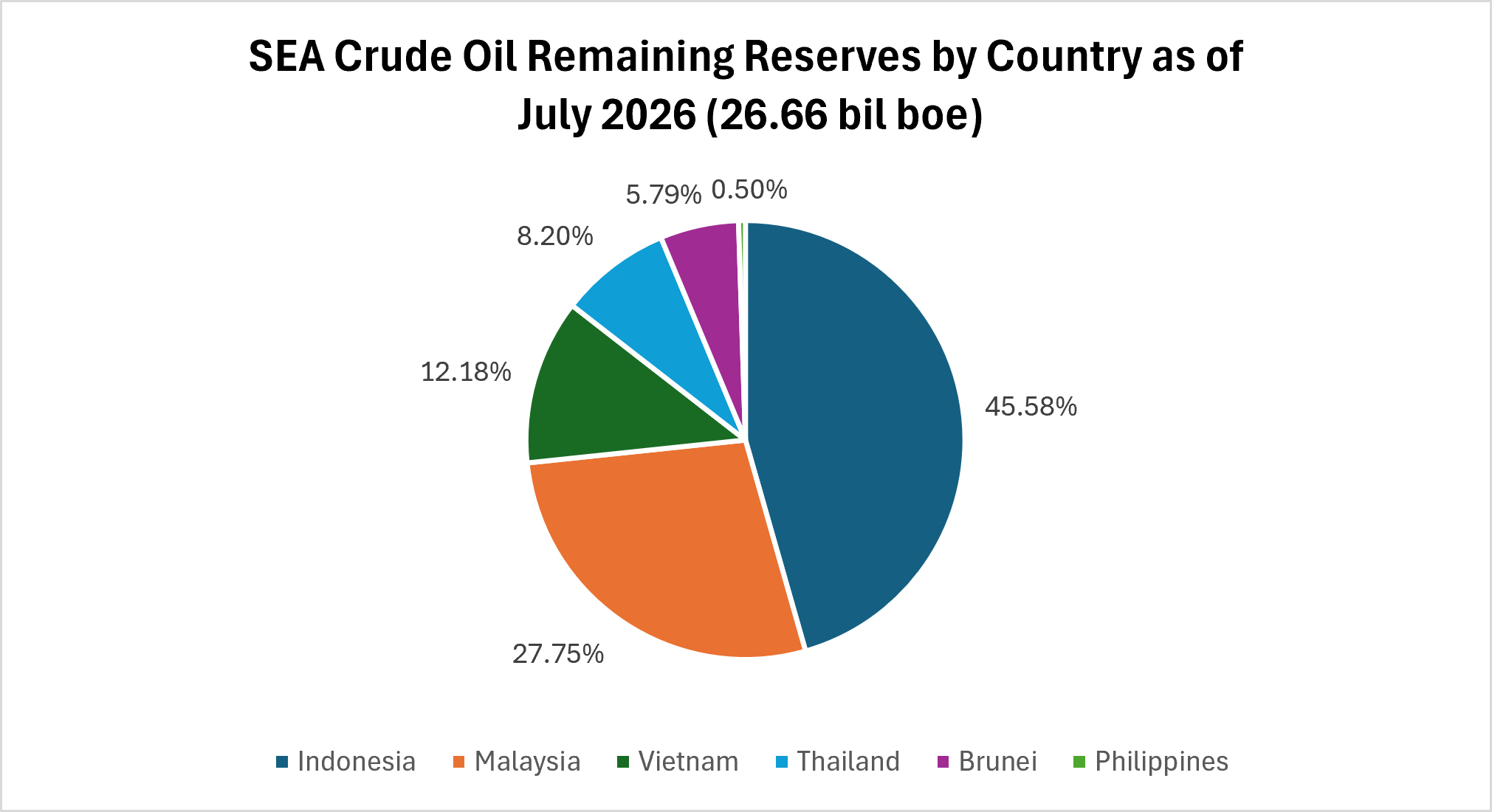

Across multiple industries food, energy, electronics, the Philippines depends heavily on imports for essential inputs. This reliance exposes the economy to global price volatility, supply chain disruptions, and currency risks. For example, energy imports make the country vulnerable to oil price shocks, while food imports raise inflation risks when global commodity prices rise. High import dependence also limits domestic value creation, as industries often stop at basic processing rather than full-scale production.

5.AI Disruption in Services

The Philippines is a global leader in business process outsourcing (BPO), employing millions in call centers and back-office services. However, rapid advances in artificial intelligence and automation are reshaping the industry. Routine customer service and data processing tasks are increasingly handled by AI, threatening low-value segments of the BPO sector.

1.Renewable Energy Opportunities

The easing of foreign ownership restrictions in the Philippines’ renewable energy sector opens strong opportunities for international investors to tap into a market transitioning toward cleaner power sources. With abundant natural resources and a government commitment to raise renewables’ share in the national energy mix to 50% by 2040, investment prospects span solar, wind, hydro, and geothermal projects, as well as green construction materials, sustainable architecture, and electric mobility infrastructure.

2.Large and Expanding Consumer Market

With a population of more than 115 million, the Philippines is one of Southeast Asia’s largest consumer markets, and its expanding middle class already nearly half the population is fueling demand for retail, food, healthcare, education, and digital products. By 2030, over 60% of Filipinos are expected to join the middle-income bracket, leading to greater purchasing power, stronger appetite for international brands and lifestyle products, and a significant shift toward online shopping and e-commerce.

3.English Proficiency and Cultural Compatibility

One of the Philippines’ most distinctive advantages is its English-speaking population. Ranked among the top countries globally for English proficiency, the Philippines provides a seamless environment for communication, marketing, and collaboration with international companies. In addition, Filipinos share cultural are tech-savvy, brand-conscious, and open to global trends. This makes it easier for foreign companies to localize products and services without facing major cultural or language barriers.

4.Young and Educated Workforce

With a median age of just 26, the Philippines boasts one of Asia’s youngest and most dynamic workforces, with over 750,000 graduates entering the labor market each year in fields such as IT, finance, engineering, and communications. This youth advantage translates into high adaptability to new technologies and business processes, competitive labor costs compared to other regional markets, and a strong foundation for service-oriented and digital industries.

5.Resilient Remittance-Driven Economy

Over 10 million Filipinos work abroad, sending home nearly USD 40 billion in remittances in 2024, which plays a vital role in supporting domestic consumption and economic stability. This steady inflow of funds strengthens purchasing power and fuels demand for real estate, retail goods, and financial services, providing businesses with a reliable source of spending activity even during global downturns. As a result, remittances make the Philippine economy particularly resilient and attractive for both local and international enterprises.

1.Leverage Liberalized Foreign Ownership Rules

Recent amendments to the Public Service Act have fundamentally changed the investment landscape by allowing 100% foreign ownership in previously restricted sectors. Foreign enterprises can now fully own operations in telecommunications, domestic shipping, railways, and renewable energy (solar and wind).

2.Capitalize on Tax Reforms and Incentive Programs

The implementation of the Corporate Recovery and Tax Incentives for Enterprises to Maximize Opportunities for Reinvigorating the Economy (CREATE MORE) Act has significantly enhanced the country’s fiscal competitiveness. The corporate income tax rate for strategic investments has been lowered, complemented by structured tax holidays and duty-free importations of capital equipment.

3.Align with National Investment Priorities

To maximize the government incentives managed by the Board of Investments (BOI) and the Philippine Economic Zone Authority (PEZA), enterprises should map their business activities against the newly updated national roadmap.

4.Optimize Logistics via Digital and E-Commerce Ecosystems

The Philippine consumer base is highly digitized, driving rapid expansion in e-commerce, digital fintech solutions, and localized fulfillment networks. Entering the market requires a robust omni-channel approach that addresses the unique logistical challenges of an archipelago.

5.Establish Strategic Distribution Networks

While foreign ownership laws have eased, partnering with established local agents remains essential for navigating retail distribution networks and domestic supply chains. Local representation is also legally mandated for foreign entities bidding on government procurement contracts.

Provides oil and gas exploration, field development, production, and management of upstream energy projects in the Philippines

Provides upstream oil and natural gas exploration, development, and production services in the Philippines and operates the Malampaya Deep Water Gas-to-Power Project, producing and supplying indigenous natural gas to power plants in Luzon

Provides oil and gas exploration, development, production, and investment in upstream petroleum projects

Provides oil and gas exploration, drilling, and petroleum development services in the Philippines

Provides engineering, construction, project management, and investment services for energy, oil and gas, and infrastructure projects in the Philippines

Provides engineering, procurement, equipment supply, and technical support services for the energy and oil and gas sectors

Provides investment, exploration, and development services for oil and gas, petroleum, natural gas, geothermal, and other energy resource projects

Provides oil and natural gas exploration, development, and production services in the Philippines as well as conducts geological and seismic surveys, manages petroleum service contracts, and develops offshore oil and gas resources

Provides engineering, fabrication, maintenance, procurement, and technical support services for the oil and gas, petrochemical, and industrial sectors

Provides drilling equipment, drilling fluids, tubular running services, well intervention, and integrated drilling solutions for the upstream oil and gas industry